Is AI creating a new economic bubble?

- Aarav Singh

- Apr 9

- 3 min read

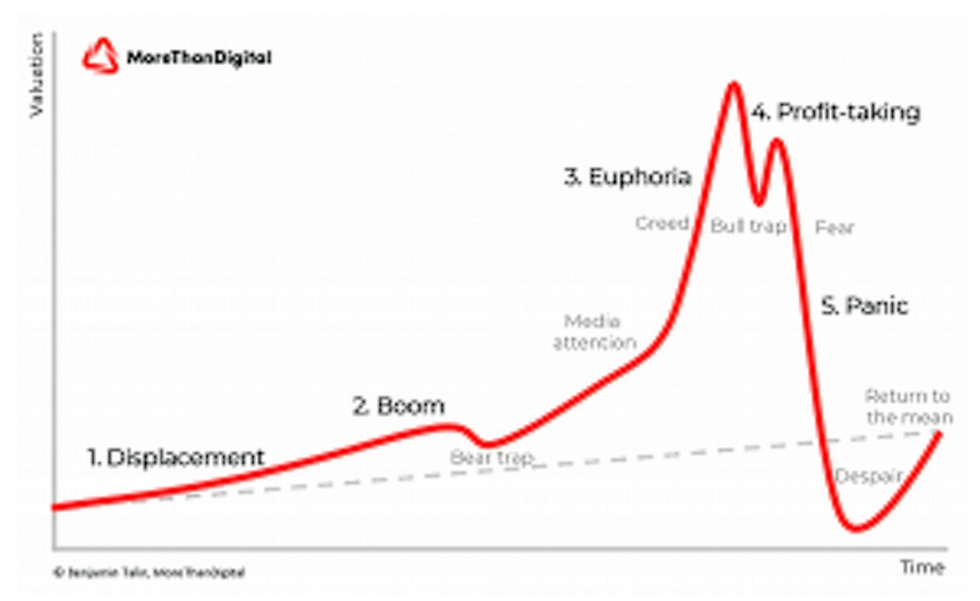

To properly understand the context of this article, defining an economic bubble is imperative. Simply put, an economic bubble is a rapid and unstable surge in the price of assets (anything from housing to books or even pets) beyond the value they hold (intrinsic value) driven by investor optimism and speculation about future success/growth from that asset. A bubble only grows as long as there is interest or positive outlooks toward the asset. The moment investor confidence shifts, the bubble is said to ‘burst’, causing a sharp drop in prices, which can lose large amounts of money.

We have had many asset bubbles in the past- famous examples including the Dot-com bubble (1998-2000, which will be looked at in-depth later) and the Real Estate bubble of the 2000s, which led to the 2008 Financial Crisis. But what has led economists to believe that Artificial Intelligence (AI) could be a bubble? The heart of this argument lies in the gap between valuations and actual profits. AI companies that manufacture chips or manage cloud or software-related production are seeing large hikes in their stock prices as a result of higher investor confidence (who are pouring in large amounts of money, driving price up) of profit explosions in the future.

The issue, however, is that current profits do not match the success that should be attained at this high of a valuation, and the reason for that is because the operational costs for AI-oriented firms is sky-high due to hefty requirements in the form of GPUs, Data Centers, and energy required to power it all. A long integration period is also why many of these AI-driven projects are not reflecting high profitability. The idea of investors to purchase AI stocks when they may be cheap (relative to what’s expected in the future) to maximize gains seems sound. However, if the profits don’t grow as they were initially projected, stock valuations will fall hard, causing major financial losses.

To better understand why economists are still weary of AI, it is best to draw parallels with the dot-com bubble in which investors poured large amounts of capital into companies whose names ended with ‘dot-com’ (.com) due to the hype and severe optimism that the internet would be able to change everything, before they even began operations or earned some profits. Both AI and dot-com companies have received large amounts of hype-driven investment, both have had large amounts of capital poured in (however, it was considered overinvestment during the dot-com bubble due to the lack of profits generated by these companies), and in both of these periods of time, companies are being given abnormal valuations, i.e. valuations that don’t match fundamental methods of pricing stocks (profits are just too low!). Even though there are commonalities between the two, differences lie in the fact that AI has established profitable giants (such as Nvidia or Microsoft), unlike the large number of small dot-com startups that lacked a product or even tangible plan in some cases, and that AI already has many use cases in the form of chatbots, customer service, or data analysis, compared to the dot-com situation where it was all largely speculative.

From this analysis, it is understood that productivity gains from the implementation of AI in industries is what will determine whether this boom is a justified long-term transformation, or whether the bubble will burst. As is obvious, investors are betting that the automation and efficiency of AI will help, however, the risk associated with this guess is that gains across firms and industries are uneven (which can lead to the setting of unrealistic expectations sometimes), materialisation of these gains may take time (employee retraining, change systems, etc.), and the high upfront cost may be difficult to cover in the short term for smaller firms (niche stocks that investors may scout as an alternative to the generic tech giants).

To conclude, the AI boom of the 2020s is suspended somewhere between speculative overvaluation and long-term beneficial transformations, and the way the scale tips is decided by the ability of AI-driven firms to deliver profits that justify market values and expectations.

Fire Article icl